The Bullish Signals Are Stacking Up

“If you don’t know where you want to get to … it doesn’t matter which way you go.” — The Cheshire Cat speaking to Alice in Alice in Wonderland

Stocks have continued to stage an impressive rally off the mid-March lows, so much so that multiple rare and potentially bullish signals have been triggered. By themselves, any one of these signals could be noise. But when they start to stack up, it may mean stocks want to move higher. And we should be ready.

- Stocks continue to stage an impressive rally off mid-March lows.

- Several potentially bullish signals are stacking up.

- Inflation eased in March, rising 5% over the past year, which is the slowest pace in nearly two years.

- Energy and food price inflation has pulled back significantly, which should be a tailwind for consumption.

- Housing inflation may also be turning a corner.

- Other areas of inflation remain hot, which will keep the Fed worried.

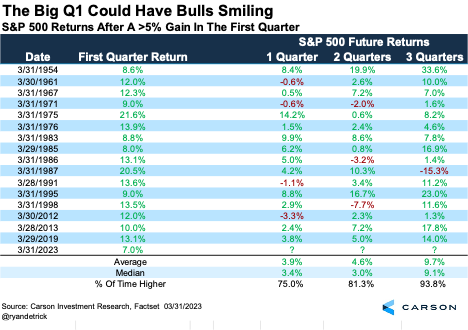

The first signal is the S&P 500 had its best first quarter since 2019, up 7.0%, which came on the heels of a 7.1% gain the previous quarter. Big first quarters often lead to continued gains. Out of 16 first quarters that gained at least 5%, the final three quarters of the year finished higher 15 times. The one outlier was 1987, which might raise a flag for some. But considering stocks were up 40% for the year by August 1987, we’ll start to worry if returns reach those heights, which we do not expect. Until then, the strong first quarter is just another clue the bulls could have a nice 2023.

The second positive sign is the overall market is being led higher by a wide range of stocks. We wrote last week how more than 93% of all stocks tracked by Ned Davis Research recently climbed above their 10-day moving averages. This rare sign of strength has led to higher prices for the S&P 500 23 out of 24 times one year later with an average return of 18.4%.

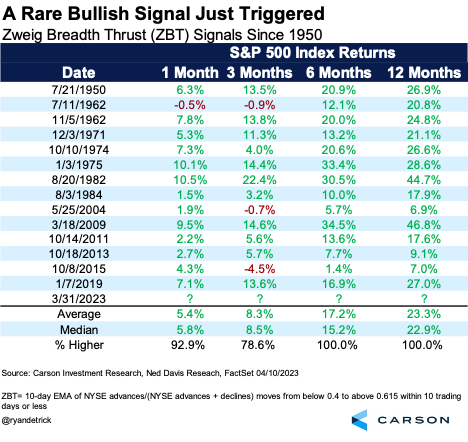

Finally, the Zweig Breadth Thrust (ZBT) indicator has been triggered, a rare and potentially bullish signal. The ZBT was coined by Marty Zweig, who is known as one of the best traders. The ZBT examines all stocks on the NYSE, tracking periods when extremely oversold stocks become extremely overbought in a short timeframe. A washout followed by heavy buying tends to open the door to higher prices.

The table below shows the previous 14 ZBTs and what followed. The S&P 500 was higher a year later every time — 14 out of 14 times and up 23.3% on average.

The Good, The Bad, The Inflation

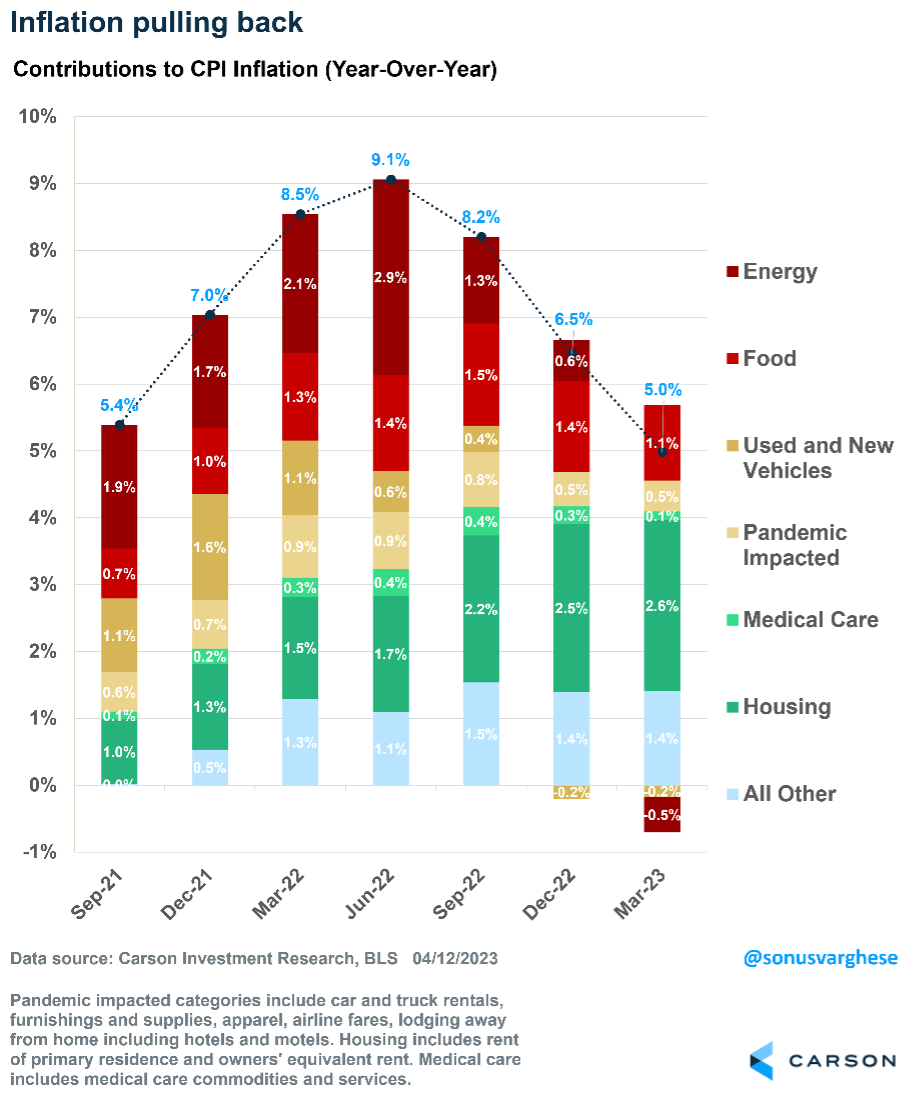

The March inflation report showed CPI inflation rose only 0.1%, slightly below expectations. Over the past year, inflation has risen 5%, well off the peak of 9% from June 2022. As the chart below shows, declining energy and food prices have pushed inflation down.

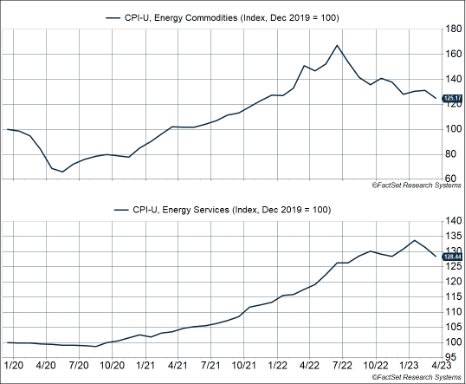

Energy makes up about 7% of the inflation basket, split almost equally into commodities, such as gasoline, and services, such as electricity and piped gas. Thanks to the pullback in oil prices, energy commodity prices are now below where they were in December 2021. The recent drop in natural gas prices has also sent services prices lower over the past couple of months.

Further good news: Prices for “food at home” i.e., groceries, fell 0.3% in March. This is the first price decline since September 2020 and bodes well for prices at restaurants, which are still elevated.

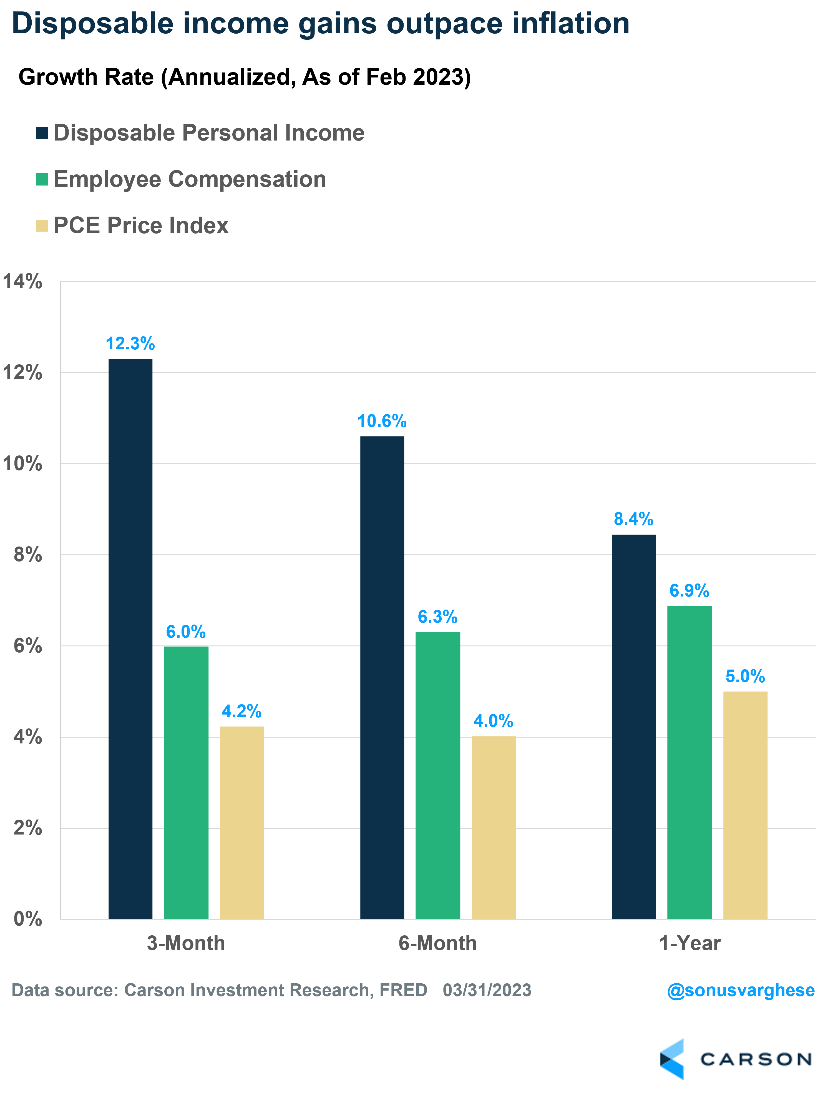

Lower Energy and Food Prices is a Big Deal for Consumption

Lower inflation, by way of lower energy and food prices, means real incomes, i.e., incomes adjusted for inflation, remain strong. Stable incomes are dependent on a healthy labor market, which appears to be holding up as we wrote here.

The chart below shows annualized growth rates of disposable income, employee compensation (across all workers in the economy), and inflation. Over the past three, six, and 12 months, disposable income has run ahead of inflation. This is partly because Social Security incomes received an inflation-adjusted boost in January. But even employee compensation is running ahead of inflation. That’s positive for consumer spending, which makes up 70% of the economy.

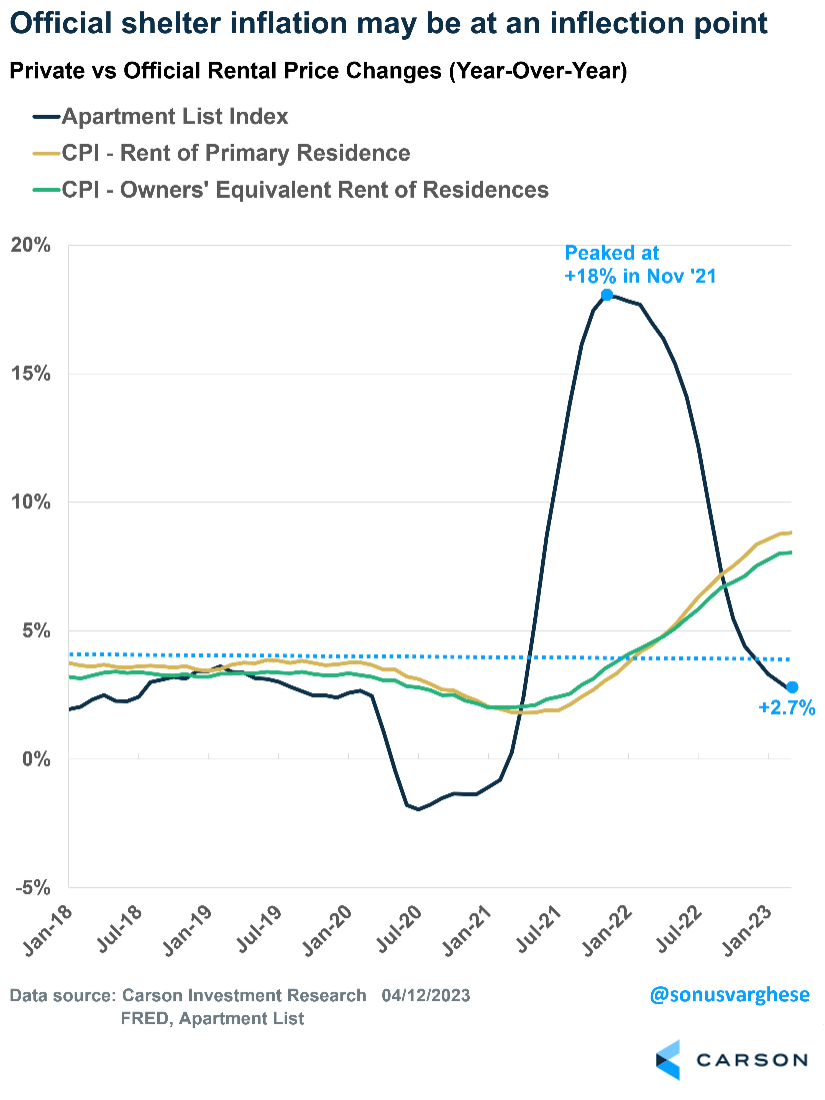

The Big Story: Housing Inflation May Finally be Falling

Core inflation, excluding food and energy, rose 0.4% in March. Over the past three months, core inflation has risen 5.1% (annualized pace) and is up 5.6% over the year. The modest slowdown is partly due to housing inflation running high.

There’s good news on that front. Rents of primary residences and owners’ equivalent rent (rental equivalent of owner-occupied homes) rose 0.5%. While still high, that pace is the slowest monthly increase in a year. Over the past nine months, housing inflation averaged about +0.7% per month, which translates to a whopping 9% annualized rate!

So, the slowdown in March is significant and most welcome.

Of course, as we’ve written about in the past, market rents have already sharply decelerated. But the official inflation data has been slow to catch up to that reality. That may be changing now, which suggests core inflation may slow down the rest of this year.

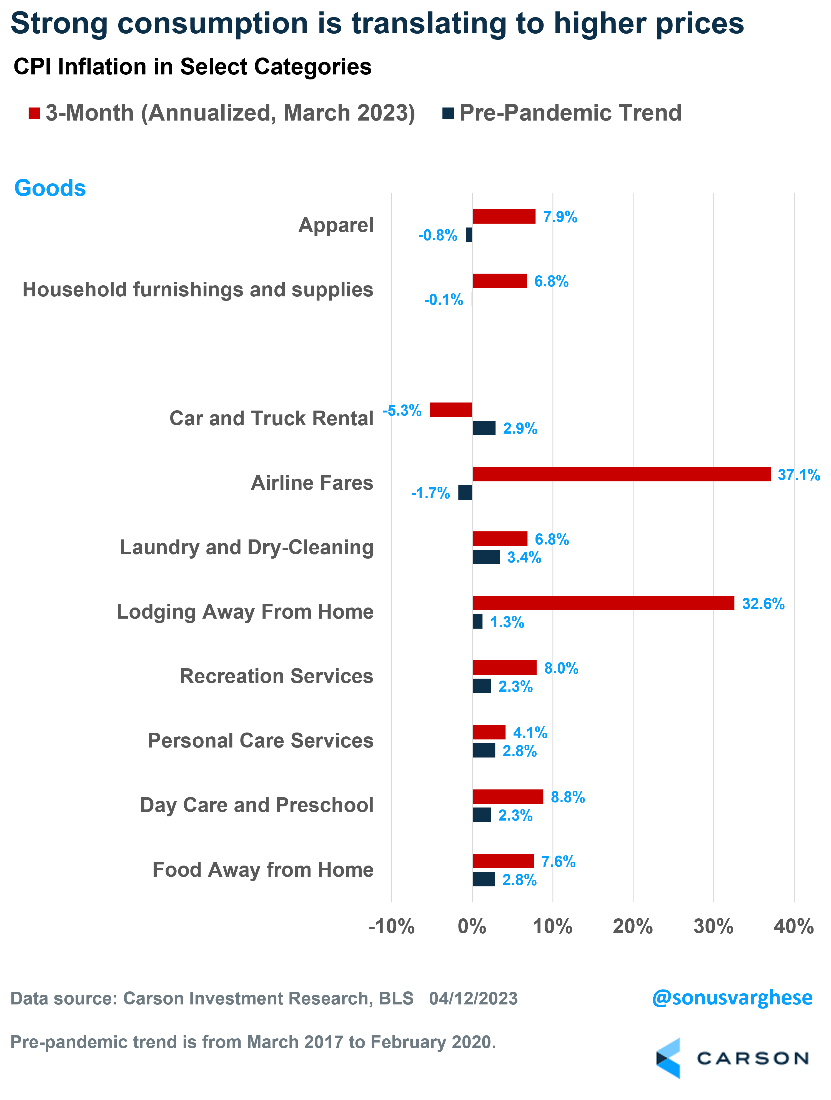

The Bad News: Core Inflation Ex Housing Remains Elevated

The slowdown in energy, food, and housing inflation is the good news. The bad news is other sectors remain elevated.

Vehicle prices are no longer falling as fast as they were. Falling vehicle prices, especially for used cars, pulled inflation lower over the last few months. In March, used car prices fell 0.9%, which is the smallest decline in seven months. Private data suggests used car prices are rising again. New vehicle prices also rose 0.4%, breaking a recent downward trend.

Outside of vehicles, many goods and services that were initially hit by the pandemic are experiencing significant price increases. These include goods, such as household furnishings and apparel, and services, such as hotels and airline fares.

Other services, such as day care, personal care, and recreation, are also seeing inflation well above pre-pandemic levels.

Stubborn inflation in these areas indicates demand for goods and services remains strong.

What Does This Mean for the Fed?

Fed officials have explicitly said they want to see core services ex housing decelerate. They’re looking at inflation excluding energy, food, and housing, the three categories that have had positive news. Unfortunately, there’s not much evidence that inflation in the Fed’s preferred category is decelerating yet. But the good news is that it tends to be correlated to wage growth, and there’s strong evidence that wage growth is moving closer to pre-pandemic levels.

The Fed is unlikely to continue raising interest rates much higher, especially since the banking crisis, which prompted caution and, as we wrote here, pushed banks to tighten credit, which is akin to rate increases. However, Fed officials are likely to keep rates where they are until they see convincing evidence of inflation falling, especially in core services ex housing.

This is not what investors expect. Investors expect the Fed to start cutting rates in late summer, pricing in at least three rate cuts by the end of 2023. That indicates bond investors believe a crisis or recession is likely in the near term, which is clearly not where Fed officials are right now. We’re not there either. We continue to believe the economy can avoid a recession.

This newsletter was written and produced by CWM, LLC. Content in this material is for general information only and not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested into directly. The views stated in this letter are not necessarily the opinion of any other named entity and should not be construed directly or indirectly as an offer to buy or sell any securities mentioned herein. Due to volatility within the markets mentioned, opinions are subject to change without notice. Information is based on sources believed to be reliable; however, their accuracy or completeness cannot be guaranteed. Past performance does not guarantee future results.

S&P 500 – A capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The NASDAQ 100 Index is a stock index of the 100 largest companies by market capitalization traded on NASDAQ Stock Market. The NASDAQ 100 Index includes publicly-traded companies from most sectors in the global economy, the major exception being financial services.

A diversified portfolio does not assure a profit or protect against loss in a declining market.

Compliance Case # 01734683