Various measures of inflation continue to track lower, likely opening a path for the Fed to stop its aggressive rate hiking cycle.

- Consumer prices continue to fall quickly, suggesting inflation is steadily trending lower.

- The consumer has been extremely strong this year, but recent retail sales data suggest the first cracks are starting to appear.

- The Fed upset the apple cart by suggesting rates would stay higher for longer, seemingly ignoring the better inflation data.

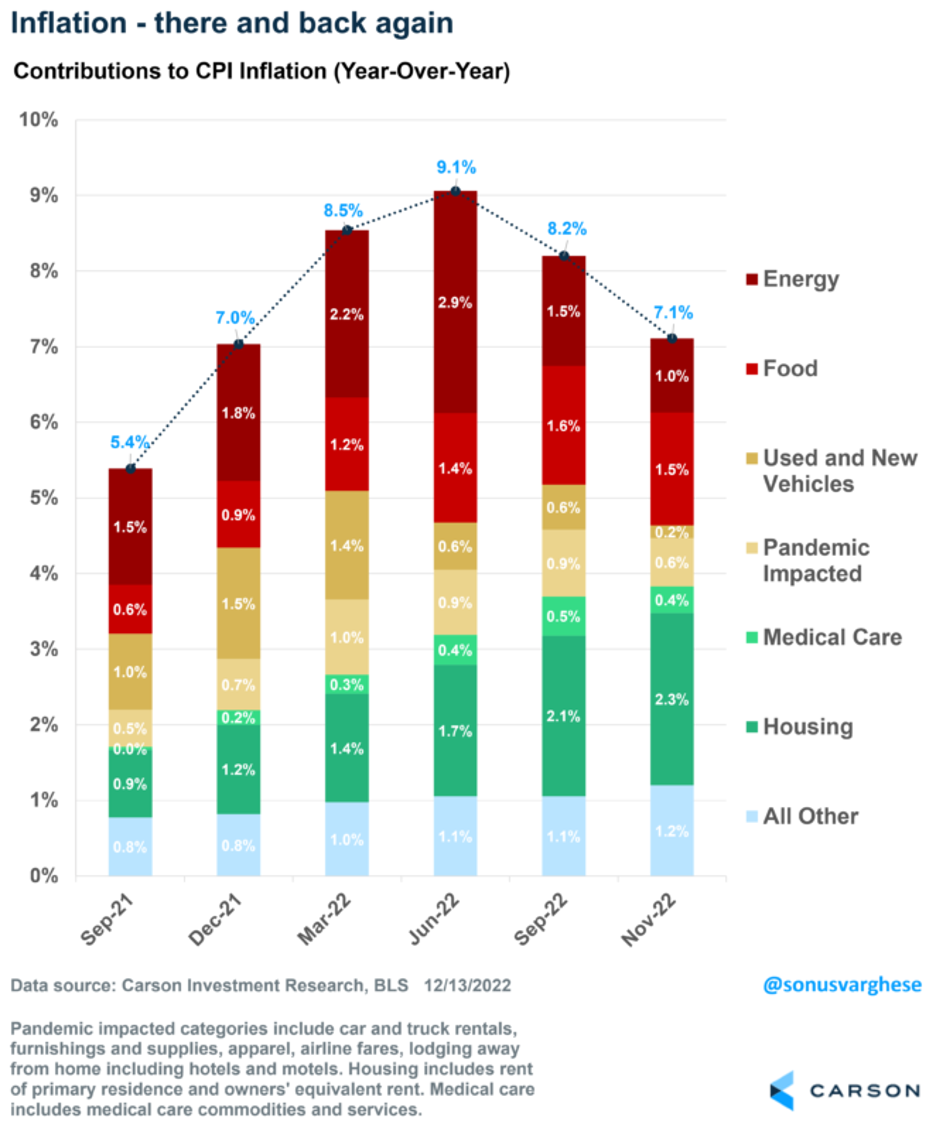

The big headline on the week was that CPI inflation came in lower than expected, the second consecutive month that consumer prices declined more than expected. Headline inflation rose 0.1% month-over-month, below expectations for a 0.3% increase and a deceleration from October’s 0.4% increase. The primary reason was energy prices, with pump prices falling 2% and prices for utility gas services falling 3.5%. Headline inflation has now pulled back from 9% in June to 7.1% as of November, which is where we were at the end of 2021. And as the chart below shows, falling energy prices (dark red bar) have contributed most to the pullback.

More highlights from the very impressive report:

- Prices for core goods, excluding food and energy, fell 0.5%. This was mostly due to used car prices, which declined by 2.9%. But also positive was that new vehicle prices were flat, which is the smallest monthly change since January.

- Medical services prices were also a deflationary force, falling 0.7%. We believe this is likely to be the case for most of next year.

- Housing, essentially rents, make up 40% of core CPI, and it looks like prices may be peaking.

- Other core services, excluding housing and medical services, were recently mentioned by Fed Chair Jerome Powell as worrying since they are tied to wage growth and wages are running hot. But a closer look at the data shows this category made its lowest contribution to core inflation in four months.

As the price for a gallon of oil has fallen to negative on the year, consumer expectations for inflation have sunk as well. A recent survey from the New York Fed found that inflation expectations going out one year are down to 5.2%, the lowest since August 2021. The Fed watches the consumer closely, and lowered expectations are a positive sign.

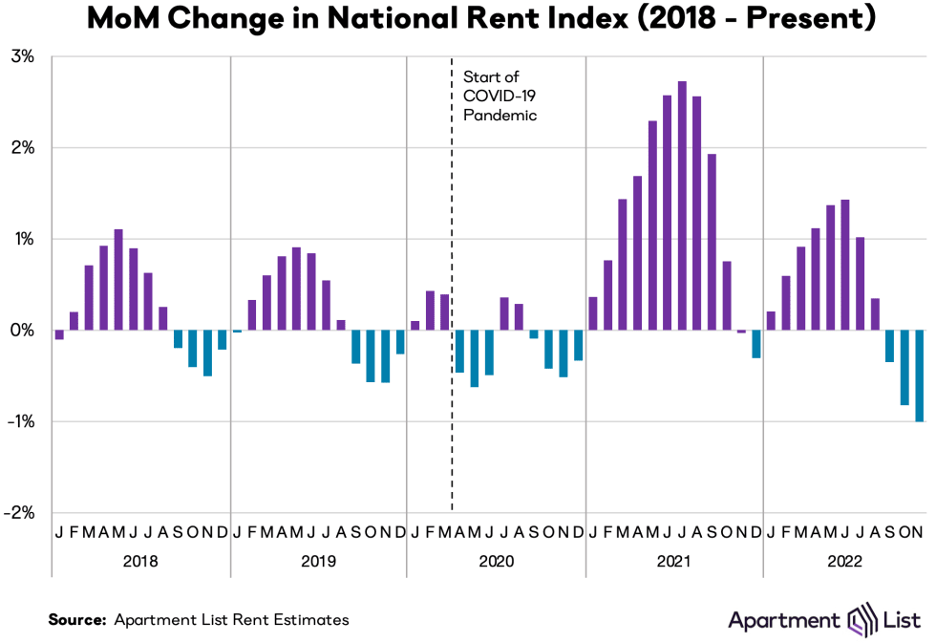

Lastly, rents are coming down at a record pace. Remember, rents make up as much as 40% of CPI, so this trend could be a major tailwind as we move into 2023, whereas it has been a headwind this year.

- Zillow data showed rent prices dropped a record 0.4% month-over-month, the largest decline ever. Meanwhile, year-over-year rent prices fell to 8.4% from the record 17.1% in February.

- Apartment List data confirmed what Zillow found, with rent prices down a record 1.0% last month, on the heels of falling 0.8% the month before.

This all matters as the government’s data shows rent prices are still increasing. But government data tends to lag private data. For this reason, lower rents will trend even lower next year as the government data catches up.

The Bad (But Not That Bad)

Retails sales for November came in with a disappointing 0.6% decline from October versus the 0.1% drop that was expected. This was on the heels of a very strong 1.3% jump in October and has many worried about the state of the consumer. Given the consumer has been the lone bright spot for the economy, any weakness here is concerning.

On the surface this was disappointing, but much of the decline was due to a very large drop in auto sales (down 2.3%) and weak online sales. Auto sales are volatile and supply chains are still causing issues here, so we’ll need to see more weakness to draw conclusions about the consumer’s strength, but we are watching it closely. Regarding online sales, some of this weakness is likely due to many consumers making online purchases earlier in the holiday season due to better deals being available sooner.

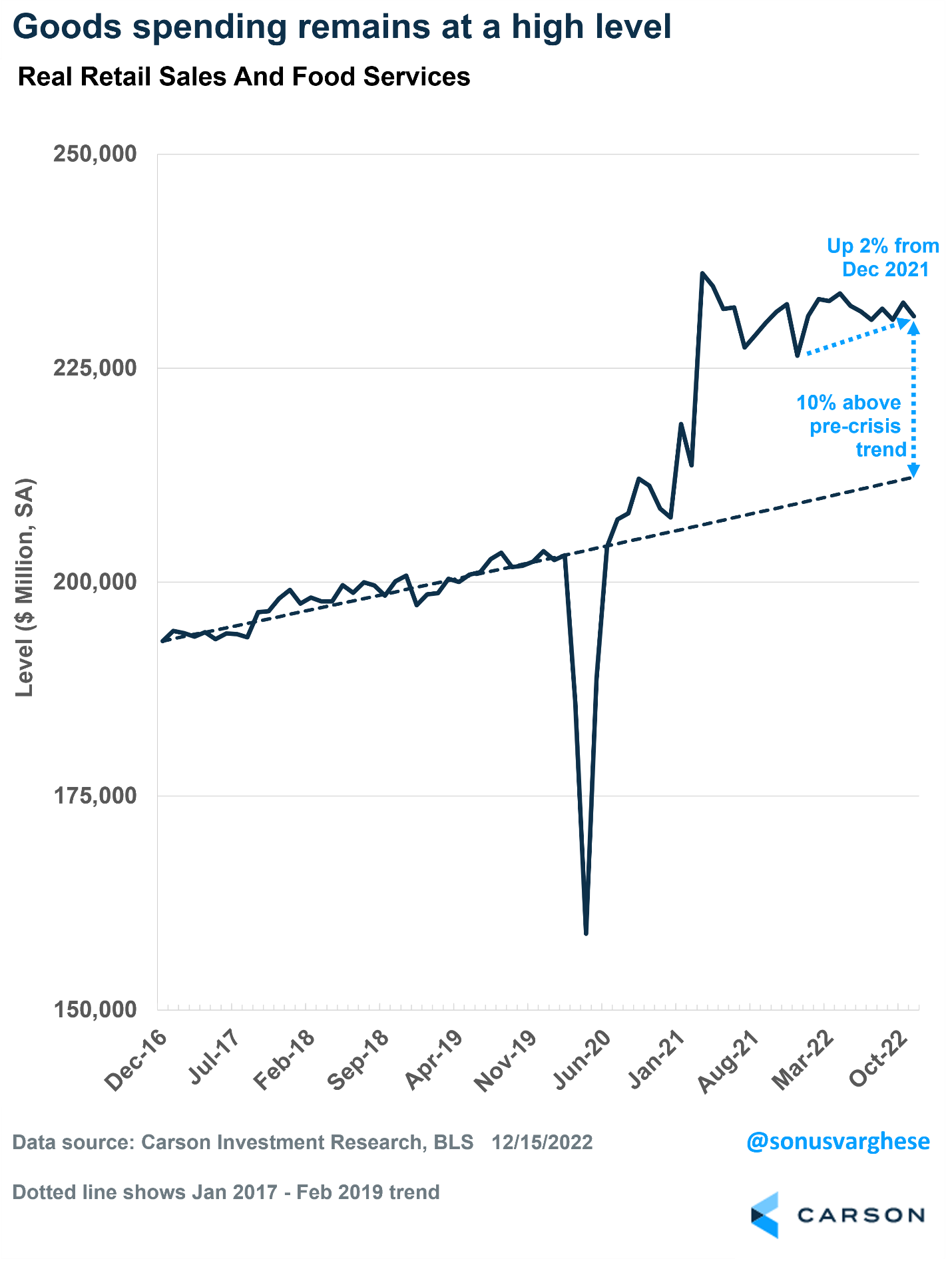

The retail sales data also showed very strong sales in restaurants and bars, up 0.9% last month and 14.1% year-over-year. So don’t count out the consumer due to one weak data point. Real retail sales (including inflation) continue to track more than 9% above the pre-pandemic trend and are up 2% for the year.

The Ugly

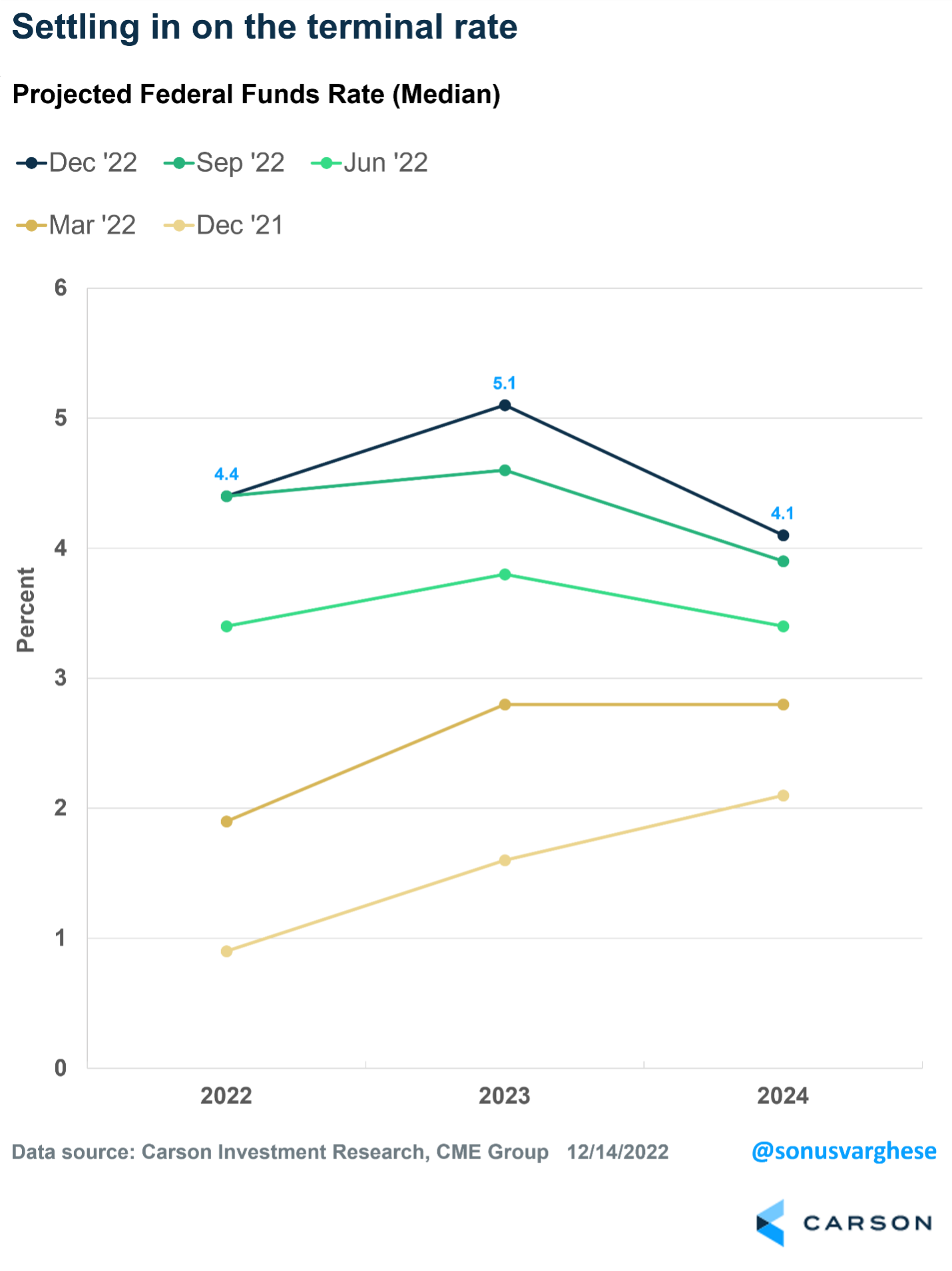

The Fed hiked rates by 50 basis points (0.50%), as expected, to a range of 4.25-4.50%, after four consecutive 75 basis point hikes. The big issue was the Fed came off more hawkish than expected, with its new estimate for a peak rate of 5.1% in 2023. The Fed also now expects GDP growth of only 0.5%, much lower than the 1.2% expected recently. Adding to the worry, Fed members now expect to see the unemployment rate climb to 4.6% next year from 4.4%.

The general takeaway from the Fed meeting was ‘higher for longer,’ and this upset the stock market and led to a large three-day selloff to end the week. Higher for longer means the Fed will keep hiking rates and will leave them there before starting to cut again. The main reason is the Fed’s continued worry about inflation. In other words, Fed members are indicating they might be OK with a mild recession if it finally puts a lid on inflation.

Here’s the catch, and there’s always a catch. This time 15 months ago, the Fed was saying inflation was ‘transitory’ and would come back down quickly. Fed officials were obviously extremely wrong here, but now they have pulled a 180 and think inflation could remain a problem in 2023, despite many signs inflation has peaked and is rolling over (goods inflation, housing, rents, medical insurance, used car prices).

There are no easy answers here, but we remain optimistic that lower inflation over the coming months will give Fed members a runway to drastically change their hawkish views. So, the question for investors will also shift — from how fast and how high to how long will they keep interest rates at an overly restrictive level? The conversation will revolve around how many months of soft inflation data is needed and how soft it must be. This could obviously take some time since inflation is not going to go down in a straight line. There may be fits and starts and false alarms, but the trend is clear.

This newsletter was written and produced by CWM, LLC. Content in this material is for general information only and not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested into directly. The views stated in this letter are not necessarily the opinion of any other named entity and should not be construed directly or indirectly as an offer to buy or sell any securities mentioned herein. Due to volatility within the markets mentioned, opinions are subject to change without notice. Information is based on sources believed to be reliable; however, their accuracy or completeness cannot be guaranteed. Past performance does not guarantee future results.

S&P 500 – A capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The NASDAQ 100 Index is a stock index of the 100 largest companies by market capitalization traded on NASDAQ Stock Market. The NASDAQ 100 Index includes publicly-traded companies from most sectors in the global economy, the major exception being financial services.

Compliance Case # 01594810