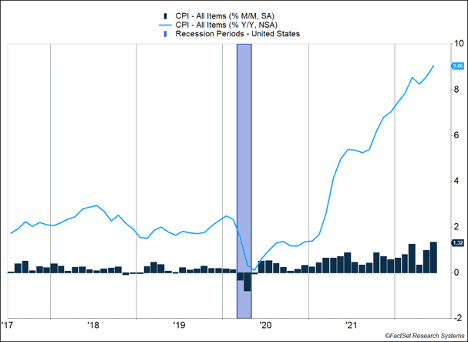

The Consumer Price Index (CPI) leapt 1.3% in June, following a 1.0% increase in May. The measure of inflation has risen 9.1% in the last year and reached its highest level since 1981 (Figure 1). Energy prices have been the top contributor in the last 12 months, responsible for 3.0% of the 9.1% annual increase. Core CPI, which excludes food and energy, rose 0.7%. Its annual level continues to slide lower, dropping from 6.0% to 5.9%. Shelter costs rose sharply as rents and housing prices pushed them higher.

Key Points for the Week

- The Consumer Price Index jumped 1.3% in June, beating expectations. Inflation has now increased 9.1% in the last year.

- Retail sales surged 1.0% as higher prices and strong employment helped retail demand stay robust in the face of higher inflation.

- Chinese GDP fell 2.6% in the second quarter. Lockdowns and a weaker property market caused the Chinese economy to shrink.

The U.S. consumer is holding up well despite the inflationary pressures. June retail sales rose 1.0% and are 8.4% higher over the last year. When adjusted for inflation, consumers are paying more for slightly fewer goods as inflation has risen faster than sales. In June, the 1.0% rise in sales lagged the 1.3% rise in inflation, and the 8.4% yearly sales gain trails the 9.1% inflation hike. For example, gasoline station sales surged 5.9% because gasoline prices were significantly higher.

Chinese GDP fell 2.6% last quarter as China’s approaches to COVID-19 restricted economic activity. The shutdowns were major contributors to retail sales falling in April and May and only partially rebounding in June. The risk of future lockdowns continues to loom large on Chinese growth and the global supply chain.

Markets were lower last week, although a rally on Friday after the retail sales report helped narrow weekly losses. The S&P 500 fell 0.9%. The global MSCI ACWI gave back 1.6%. The Bloomberg Aggregate Bond Index rallied 0.9%. The Job Openings and Labor Turnover Survey as well as second quarter earnings are the key data points likely to move markets this week.

Figure 1

Inflation Spirals Higher

U.S. inflation continued to run higher in June. A monthly increase of 1.3% added to already high inflation and pushed the yearly inflation rate to 9.1%. As we shared last week, pay increases have been most rapid for those with the least education and lowest-paying jobs. While these pay gains have helped, this group is also the most vulnerable to increases in inflation as they spend a higher percentage of their incomes on basic goods and have less spending flexibility than higher earners.

Energy costs have contributed significantly to annual inflation. Although energy makes up only 7% of the basket of goods used to measure CPI, it has contributed 3.0% to the yearly inflation rate, accounting for nearly one-third of the increase. When combined with food and auto prices, the three categories contributed 56% of the inflation, yet make up only 28% of the basket. Any relief in these areas could help slow inflation.

The details of the report provided little positive news. A few travel categories reported lower prices, but those have still increased by more than the overall CPI average in the last year. A plethora of categories climbed more than 0.5%, suggesting inflation pressure continues to broaden.

Some relief on energy prices will help next month’s report. Gasoline prices have declined for more than 30 straight days, after peaking in early June. Because the average price in June was above May’s average, gasoline pumped inflation higher in June. That should reverse in July. Some factors working in the opposite direction will make next month’s inflation a tougher comparison. Monthly inflation ebbed lower in the third quarter last year, and that means smaller monthly increases may still push the annual inflation rate higher than the already high 9.1%.

The Federal Reserve meeting in two weeks is the next big event in the ongoing fight to lower inflation. In its recent minutes and subsequent press appearances, Fed governors have gone out of their way to make up for being overly optimistic about inflation trends earlier. Since dropping “transitory” from its description of inflation late last year, the Fed has become more hawkish, meaning it has more will to raise rates. That hawkishness, combined with the big jump in CPI, has cemented expectations for at least a 0.75% increase in interest rates later this month. Some have begun to forecast an increase of 1.0%, matching the Canadian central bank’s recent hike.

A 1.0% increase seems a big step given the moves already made by the Fed and others. Even amid the high inflation, strong employment environment, and solid retail sales, there are signs the global economy is slowing. The International Monetary Fund (IMF) announced it will reduce its projections for economic growth for the second time in three months due to the ongoing war in Ukraine, higher inflation, and ongoing supply bottlenecks. Some Fed governors are counselling against raising rates too fast. Esther George, who leads the Federal Reserve Bank of Kansas City, worries, “…that a rapid pace of rate increases brings about the risk of tightening policy more quickly than the economy and markets can adjust.”

Interest rate hikes often slow the economy after a lag, as some economic momentum takes a while to reverse. The U.S. is not alone in raising rates. The U.K., South Korea, Canada, and Australia have all increased rates, which will help slow global activity. According to the IMF, 75 central banks have raised interest rates since July 2021.

Perhaps a useful analogy for the Fed’s current challenge is someone trying to train for a marathon after sitting on the couch for most of the pandemic and then postponing the start of the training program until long after the recommended start date. The erstwhile marathon runner will have to accelerate her training much more rapidly to get in good enough shape to finish the race. At the same time, the intense training regimen required increases the chance of injury. The Fed is in a similar situation. Having waited too long to start increasing rates, it finds itself having to walk a narrow path between pushing too hard and not pushing hard enough.

Based on the signals the Fed is giving, we expect it will increase rates 0.75%. That attempts to balance the goal of taking big steps to curtail inflation while still giving the economy and markets time to adjust to a higher rate environment.

–

This newsletter was written and produced by CWM, LLC. Content in this material is for general information only and not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested into directly. The views stated in this letter are not necessarily the opinion of any other named entity and should not be construed directly or indirectly as an offer to buy or sell any securities mentioned herein. Due to volatility within the markets mentioned, opinions are subject to change without notice. Information is based on sources believed to be reliable; however, their accuracy or completeness cannot be guaranteed. Past performance does not guarantee future results.

S&P 500 INDEX

The Standard & Poor’s 500 Index is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

MSCI ACWI INDEX

The MSCI ACWI captures large- and mid-cap representation across 23 developed markets (DM) and 23 emerging markets (EM) countries*. With 2,480 constituents, the index covers approximately 85% of the global investable equity opportunity set.

NBC News. Laura Eagan. 07/17/2022. https://www.nbcnews.com/politics/gas-prices-are-falling-voters-say-arent-feeling-relief-rcna37680

IMF. Kristalina Georgieva. 07/13/2022. https://blogs.imf.org/2022/07/13/facing-a-darkening-economic-outlook-how-the-g20-can-respond/

Wall Street Journal. Nick Timaros. 07/17/2022. https://www.wsj.com/articles/fed-officials-preparing-to-lift-interest-rates-by-another-0-75-percentage-point-11658068201?mod=hp_lead_pos1

Wall Street Journal. Michael S. Derby. 07/11/2022. https://www.wsj.com/articles/feds-george-concerned-about-effect-of-aggressive-rate-rises-on-economy-11657554589?mod=article_inline

Cheddar News. Alex Vuocolo. 12/15/2021.0 https://cheddar.com/media/fed-chair-powell-drops-transitory-from-statement-speeds-up-taper#:~:text=Fed%20Chair%20Powell%20Drops%20’Transitory’%20From%20Statement%2C%20Speeds%20Up%20Taper,-Dec%2015%2C%202021&text=As%20prices%20for%20goods%20hit,in%20its%20latest%20policy%20statement

US Bureau of Labor Statistics. 07/13/2022. https://www.bls.gov/news.release/cpi.nr0.htm

US Census Bureau. 07/15/2022. https://www.census.gov/retail/marts/www/marts_current.pdf

CNBC. Evelyn Cheng. 07/14/2022. https://www.cnbc.com/2022/07/15/china-q2-gdp.html

Compliance Case # 01432458